US ECONOMY

Economic growth moderated in the second quarter as falling fixed investment and a weak external sector dragged on growth. Nevertheless, American consumers continued to buttress growth in Q2, with household spending rising robustly over the quarter, and this trend has likely continued into Q3. In July, retail sales were surprisingly strong, consumer confidence recovered and the jobs report highlighted a healthy labor market. That said, the manufacturing sector slowdown persisted in the same month, with the ISM index falling to a near three-year low, weighed on by waning external demand amid the ongoing trade dispute with China. With regards to the latter point, the recent escalation in trade tensions suggests a swift resolution to the trade war is highly unlikely, which will drag on growth ahead and could prompt the Federal Reserve to further loosen monetary policy.

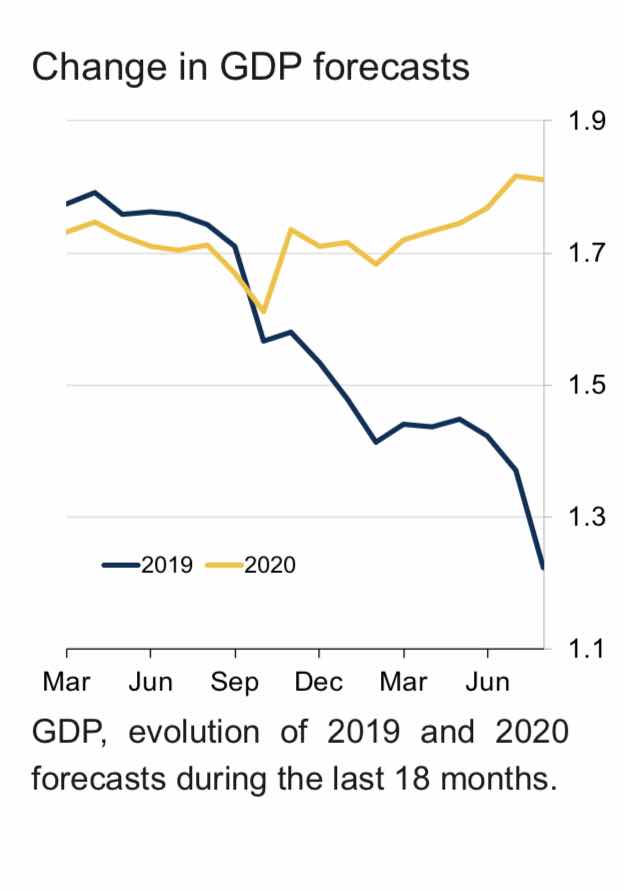

While economic growth seems set to ease in H2, with a weaker global outlook and the ongoing U.S. - China trade dispute weighing on business investment, manufacturing and exports, resilient consumer spending and lower borrowing costs should cushion any slowdown.

The key downside risks stem from a prolonged trade row and high corporate debt.

Inflation rose to 1.8% in July from 1.6% in June, signaling the trade war could be feeding into price pressures. Underlying inflation also edged up in the month. Inflationary pressures are expected to pick up slightly in the quarters ahead, on strong domestic demand and supply-side pressures due to tariffs.

At its meeting in July, the Fed cut its target range to 2.00%–2.25% but stressed it was a policy adjustment rather than the start of an easing cycle. Nevertheless, the recent escalation in trade tensions has prompted many of our panelists to pencil in another 25-basis-point rate cut at the 17-18 September FOMC meeting. FocusEconomics panelists expect the federal funds rate to end 2019 at 1.95% and 2020 at 1.77%.

TRADE RELATIONS

U.S.-China trade war heats up with new round of tit-for-tat tariffs Trade tensions escalated to unprecedented levels in recent weeks, with a fresh round of tit-for-tat tariffs from both the U.S and China increasing concerns that the over year-long trade war will persist beyond 2019. This will likely weigh on U.S. growth going forward. On 1 August, U.S. President Trump triggered an escalation in trade tensions when he abruptly announced that a 10% tariff would be slapped on the remaining USD 300 billion of imports from China not currently subject to tariffs. A few weeks later, Trump partially backed down by postponing some tariffs on a list of consumer goods from September to December, likely to ensure the tariffs would not dampen consumer spending—the mainstay of the economy—ahead of the critical Christmas buying season. The threat to impose tariffs on all remaining imports followed President Trump’s supposed dissatisfaction with the quantity of American agricultural goods that China was buying and the lack of progress being made in trade negotiations. On 23 August, China retaliated with its own tariffs ranging from 5% to 10% to be imposed on USD 75 billion worth of U.S. goods, and to be implemented in two phases matching the dates of Trump’s tariffs.

This followed the decision by the People’s Bank of China to allow the yuan to fall below the symbolic 7-yuan-per-dollar mark in early August, prompting the U.S. to label China a currency manipulator. The levies will specifically target goods including soybeans, crude oil and light aircraft, and China said it will also reinstate a 25% tariff on U.S cars and a corresponding 5% duty on auto parts in December. The retaliation thus clearly targets products linked to Trump’s core constituents in the industrial and agricultural belts, which are considered key swing states ahead of next year’s presidential election. As summarized by Iris Pang, greater China economist at ING, “it won’t have escaped the Chinese authorities’ attention that a full-blown trade war is unlikely to help President Trump’s chances in the election.” Hours later Trump announced a new set of countermeasures, stating the U.S. would raise the planned tariffs on USD 300 billion worth of Chinese goods that are scheduled to come into effect in September and December from 10% to 15%, while also increasing the existing tariffs on USD 250 billion worth of Chinese imports from 25% to 30% on 1 October.

Report from: FocusEconomics Consensus Forecast Major Economies

Cartoon by Pavel Constantin, Romania

Follow Us

Sign up for updates and new posts by email!!!!