The political standoff between President Nicolás Maduro and Juan Guaidó, who declared himself interim president on 23 January and has been recognized as such by more than 50 countries, is far from over. Following the unsuccessful attempt by Guaidó and his allies to deliver aid into the country on 23 February, the opposition leader embarked on a support-seeking tour across the region before returning to Venezuela without incident on 4 March, despite breaking a court-imposed travel ban, to continue pressing on President Maduro to step down. Meanwhile, the diplomatic and economic pressure continues to mount as the U.S. announced new sanctions targeting high-profile figures in the Venezuelan government and military. This follows the painful sanctions imposed on the all-important oil industry in late-January, which have led government officials to scramble in seeking alternative markets to sell crude and securing access to its gold reserves as well as much-needed foreign currency. The latest power outages, which have been running for nearly a week, complicate matters further as they are set to impact oil operations and disrupt day-to-day economic activity.

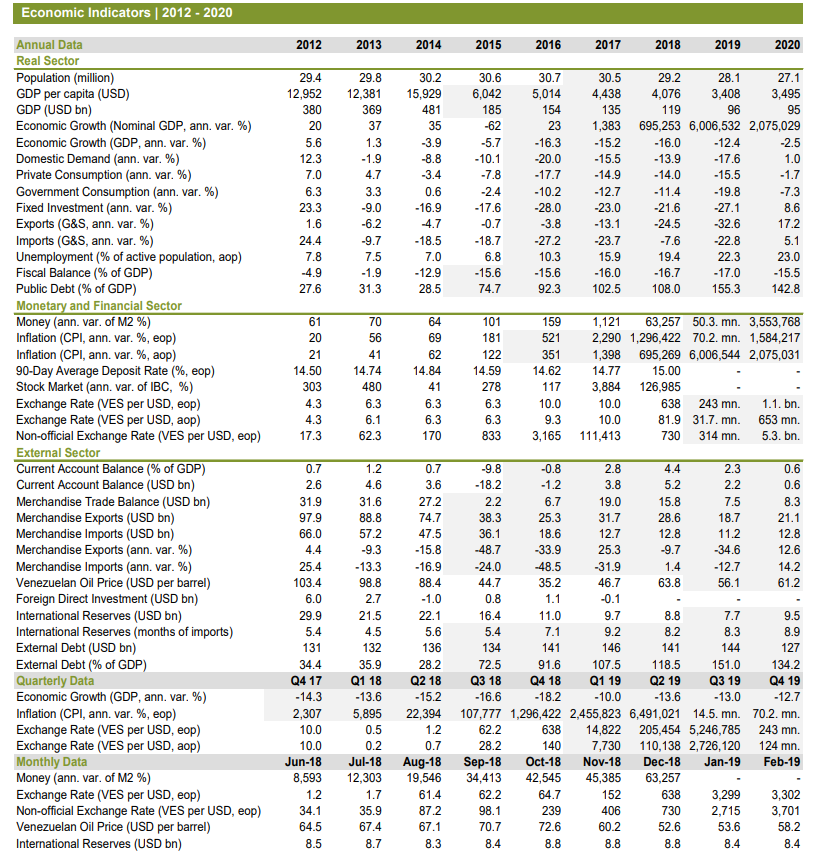

The outlook is grim. On the one hand, the political situation remains in limbo, with the Maduro government likely opting to wait out the crisis while Guaidó strives to keep up the momentum. On the other hand, financial sanctions aimed at choking off the government’s access to external financing and its oil revenues inflict more damage to an already crippled economy besieged by run-away inflation and goods shortages. The possibility of political change has increased amid the latest events, a scenario which some of our panelists have factored into their forecasts. FocusEconomics panelists see the economy contracting 12.4% in 2019, which is down 2.1 percentage points from last month’s forecast. In 2020, the panel sees GDP falling 2.5%.

Panelists estimate inflation to have ended 2018 at nearly 1,300,000%. Last year’s monetary reconversion has been unable to tame hyperinflation while sanctions are set to worsen goods scarcities going forward, further fueling inflationary pressures. Our panel sees inflation surging to over 70,000,000% by the end of 2019, before falling to around 1,500,000% by the end of 2020. Despite the sharp devaluation of the currency in late-January which brought the official rate roughly up to par to the black market’s, the differential between the two has started to widen yet again. The official DICOM exchange rate came in at 3,300 VES per USD in the 8 March auction, while the parallel market rate fell to 3,603 VES per USD that same day. Our panelists expect the official rate to end 2019 at 243 million VES per USD, before rising to 1.1 billion VES per USD by the end of 2020.