The outlook in Turkey has worsened.

Economics

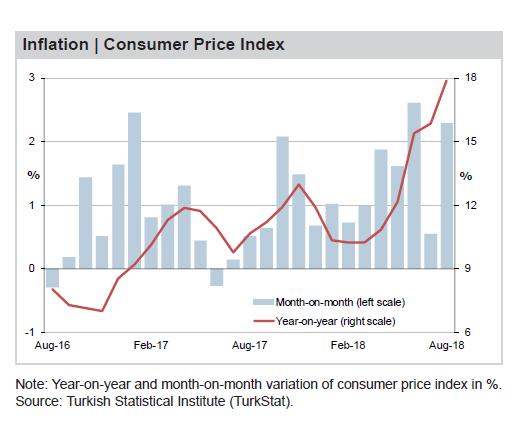

Recent indicators suggest the economy slowed sharply in the third quarter. Consumer and business confidence continued to plummet in September and are now both firmly in negative territory, while in the same month the manufacturing PMI sank lower on stronger contractions in output and new orders. Moreover, annual retail sales growth reached an over one-year low in July. Retail sales likely softened further in the remainder of Q3, on higher inflation and weaker sentiment. On the plus side, the gaping current account deficit has begun to narrow thanks to the weaker currency and softer domestic demand. This comes after recent figures show that growth held up well in the second quarter, buoyed by a stronger external sector, a pre-election government spending boost and robust private consumption. On the political front, in late September Treasury and Finance Minister Berat Albayrak, presented the much-anticipated New Economic Plan, which sets out a more constrained fiscal stance and far lower growth forecasts. • The economy will likely lose considerable steam in the next few quarters on tight financial conditions, weak sentiment and sky-high inflation. Further exchange rate volatility and an escalation of geopolitical tensions pose significant downside risks. FocusEconomics panelists expect growth of 3.6% this year and 1.0% in 2019, down 2.0 percentage points from last month’s forecast. • Inflation rose from 15.8% in July to 17.9% in August, pushed up by the weaker lira. Inflation is likely to rise even further in the coming months given the recent currency crash but should then dip on softer domestic demand. Our panel sees inflation ending 2018 at 20.7% and 2019 at 13.7%. • At its 13 September meeting, the Central Bank jacked up the repo rate from 17.75% to 24.00%. The decisive move was designed to support the currency and temper price pressures, and it should go some way to restoring investors’ faith in the Bank’s independence. The Bank is likely to maintain its tight stance in the near-term to consolidate recent lira gains and check runaway inflation. Our panelists see the one-week repo rate ending 2018 at 24.25% and 2019 at 19.97%. • On 28 September, the lira traded at TRY 6.06 per USD, strengthening 3.5% from the same day in the previous month. The appreciation followed announcements of tighter fiscal and monetary policy. Nevertheless, the currency has still lost a huge amount of value since the start of the year. Going forward, the lira is likely to remain highly volatile, due to geopolitical tensions with the U.S. and ongoing market skepticism of the government’s policy agenda. Our panelists see the exchange rate ending 2018 at TRY 6.46 per USD and 2019 at TRY 6.73 per USD at end-2019.

Politics

Treasury and Finance Minister Berat Albayrak presented the New Economic Program (NEP) (formerly the Medium-Term Program, MTP) on 20 September. The plan provided more credible macroeconomic forecasts—including for reduced growth and markedly higher inflation—and set out a more cautious fiscal stance. As a result, the program should go some way to restoring investors’ faith in the government’s macroeconomic policymaking, reduce economic imbalances and support the lira. However, full implementation of the announced measures will be key to rebuilding investors’ trust, while concrete proposals for the banking sector were limited. The program established TRY 60 billion of cost savings and TRY 16 billion of extra revenue for 2019 (around USD 12 billion in total). The vast majority of cost savings are expected to come from investment programs, incentives and

the social security system, while extra revenue will be raised by broadening the tax base through a reduction in exemptions. The government also announced changes to public-private partnership (PPP) initiatives to boost affordability. This comes after the IMF warned the country earlier this year

about the fiscal risks associated with such schemes, which have played a key role in infrastructure development under President Erdogan and were recently valued by the Fund at around USD 61 billion. Thanks to this fiscal austerity, the NEP forecasts a rising primary surplus and a central budget deficit contained below 2% of GDP going forward. Moreover, the plan sees the economy growing just 2.3% next year and 3.5% in 2020, in contrast to a target of 5.5% growth in both those years in last year’s MTP.

The 2019 target is still markedly above FocusEconomics panelists’ expectations, but the overall message is that—at least in the near-term—President Erdogan appears willing to temper his growth-at-all-costs approach to economic policymaking. Regarding inflation, the plan sees it ending next

year at around 16%, and only returning to single digits in 2020. Looking at the external sector, the government aims to sharply reduce the current account deficit going forward. As well as the weaker lira aiding competitiveness, the program also aims to achieve this by boosting domestic production in areas such as pharmaceuticals, energy and machinery, where Turkey is currently extremely dependent on imports. This will take time, however, and FocusEconomics panelists predict a more modest narrowing of the current account deficit over the coming years. Regarding the banking sector, the NEP stated that the government will conduct a review of banks’ financial soundness. However, there were no concrete steps to address concerns over non-performing loans—which could rise as firms struggle with a hefty external debt burden—or banks’ access to international financing. According to ING analysts, the “programme is a step in the right direction with rebalancing on growth and reviving a commitment to fiscal prudence, though the inflation path is to remain elevated longer.”

Economists at Nomura also agree that the NEP—together with the Central Bank’s recent rate hike—is a sign that “the authorities are gradually adjusting to reality.” However, they go on to state: “We do not believe they [the NEP and rate hike] are enough to reverse the long-running trend of erosion of policy making credibility in Turkey. Even if these are credible policy changes, it is probably too late to reverse the economic downturn because of the negative effects of currency depreciation on private sector balance sheets.” The more conservative fiscal stance should provide support to the beleaguered lira going forward. However, ING and Nomura highlight that the Plan’s implicit 2019 exchange rate assumption—calculated by both firms at around TRY 5.60 per USD—could be slightly optimistic. FocusEconomics panelists concur, and see the currency ending 2018 at TRY 6.46 per USD and 2019 at TRY 6.73 per USD. Despite tighter fiscal and monetary policy, a sustained improvement in the exchange rate outlook will likely be dependent on a reduction in geopolitical tensions, particularly a normalization of relations with the United States. As economists at Nomura comment: “We also need a de-escalation on the foreign policy front. […] If there is no resolution […] and if this is followed by further US sanctions on Turkey (and a possible fine on state-owned Halkbank), then the pressure on Turkish assets will resume forcefully.”