The economy likely contracted at an even sharper pace in the second quarter as Covid-19 induced lockdowns weighed heavily on activity. In May, the unemployment rate ticked down from April’s near 40-year high, but was still roughly 10 percentage points higher than its pre-crisis level. Moreover, despite jobless claims dipping slightly in recent weeks the number of people receiving benefits was over 15% of the labor force, which will be hammering private consumption. Meanwhile, although the downturn seems to have bottomed out, some parts of the country have tightened restrictions as the seven-day moving average of daily new Covid-19 cases accelerated in recent days, boding ill for hopes of a smooth economic recovery. Furthermore, a re-emergence of tensions with China has fueled market uncertainty in recent weeks and could lead to a new round of escalation.

The economy will shrink notably this year. Elevated unemployment will suppress consumer spending, while investment and trade are set to decline. Fiscal and monetary stimulus should help cushion the blow, however. A second wave of infections and tensions with China are key risks.

At its 9–10 June meeting the Fed maintained the target range at its effective floor of 0.00%–0.25%. More importantly, the FOMC reaffirmed its commitment to employing its full range of policy tools to mitigate the economic fallout and spur a recovery. The next meeting is set for 28–29 July. Our panelists project the federal funds rate to end 2020 at 0.25% and 2021 at 0.28%. The dollar index dipped over the past month as economic conditions continued to improve globally, which raised investors’ risk appetite. On 26 June, the dollar index traded at 97.2, depreciating 2.6% month-on-month. The evolution of the Covid-19 pandemic will continue to determine the dollar’s performance moving forward.

REAL SECTOR

ISM manufacturing index picks up from 11-year low in May The Institute for Supply Management (ISM) manufacturing index increased from 41.5 in April to 43.1 in May, virtually meeting market expectations of 43.0. Nevertheless, the index remained below the 50-threshold that separates contraction from expansion in the manufacturing sector. May’s result was driven by softer deteriorations in new orders, production and employment, but remained sharp nonetheless. Moreover, new export orders and backlogs of work also declined at a weaker pace in May relative to April. The first quarter’s contraction is likely just the tip of the iceberg in terms of the economic impact of the pandemic. While unprecedented fiscal and monetary stimulus should soften the blow, FocusEconomics panelists project the economy to contract in Q2 at the sharpest rate since the Great Depression. Extensive damage to the labor market—with over 40 million Americans recently having filed for unemployment benefits—will be hitting private consumption hard. Moreover, lockdowns abroad will be weighing on exports. Looking ahead, the manufacturing sector will likely remain subdued as anemic economic activity weighs on demand. Moreover, recent social unrest, which resulted in lockdown measures—unrelated to the virus outbreak—poses a downside risk to domestic demand for U.S. manufactured goods. FocusEconomics Consensus Forecast panelists expect industrial production to decline 9.2% in 2020, which is unchanged from last month’s forecast.

In 2021, panelists see industrial production rising 5.2%. FocusEconomics Consensus Forecast panelists expect GDP to contract 5.6% in 2020, which is up 0.2 percentage points from last month’s estimate. For 2021, the panel expects the economy to expand 4.6%.

REAL SECTOR

Retail sales jump at the fastest pace on record in May Nominal retail sales surged at the fastest rate in the series’ near three-decade history in May, jumping 17.7% in month-on-month seasonally-adjusted terms. The result contrasted April’s 14.7% plummet and was significantly better than market expectations of an 8.0% increase. Retail sales excluding cars, gasoline, building materials and food services—also known as core retail sales—soared 12.4% in May, rebounding from April’s 15.2% plunge. The historic rise in retail sales came as large sections of the country eased lockdown restrictions. Retail sales of clothing and accessories skyrocketed 188.0% month-on-month in May (April: -75.3% month-on-month). Moreover, retail sales of food services increased notably as restaurants came back online in May, while purchases of sporting goods, furniture, electronics and motor vehicles all surged in May after contracting sharply in April. In annual terms, retail sales declined 6.1% in May, considerably softer than April’s 19.9% dive. Meanwhile, the annual average variation in retail sales growth fell to 0.4% from 1.2%. Lastly, for the first five months of the year retail sales were down 4.7% compared to the same period last year, but were down 10.5% in March–May—the start of the pandemic—compared to the same three months last year. Commenting on May’s reading, Sri Thanabalasingam, an economist at TD Economics, noted: “One-time checks and expanded unemployment insurance, provided by the CARES Act, has more than offset losses in employment income for most households. This helped support the rebound in retail sales. With expanded unemployment payments set to expire in July, households could see a significant drop in income if unemployed members have not returned to work. The turnaround in the labor market in May was promising, but if it stalls, Congress should stand ready to provide additional support to American households.” FocusEconomics Consensus Forecast panelists see private consumption falling 5.8% in 2020, which is up 0.5 percentage points from last month’s forecast.

REAL SECTOR

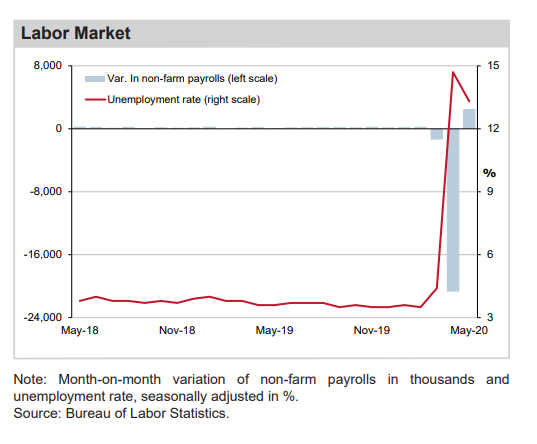

Labor market unexpectedly posts gains in employment in May Total non-farm payrolls surged 2.5 million in May, increasing at the sharpest rate since the series began in 1939, and baffled market analysts’ expectations of an 8.0 million decline. This follows April’s 20.7 million payroll cut—the starkest on record—driven by the Covid-19 pandemic and measures to contain the virus. Employment in the leisure and hospitality, construction and retail sectors increased notably in May, as containment measures gradually eased. The unemployment rate decreased to 13.3% in May from 14.7% in April, while the labor force participation rate ticked up from 60.2% in April to 60.8% in May. Hourly earnings fell 1.0% month-on-month in May (April: +4.7% monthon-month), while annual wage growth decelerated from 8.0% in April to 6.7% in May. Despite a positive reading in May, total non-farm payrolls are still down nearly 20 million since February. Going forward, the labor market should gradually improve as lockdown measures continue to ease, but our panelists expect the unemployment rate will remain elevated for the remainder of this year.

Commenting on May’s reading, James Knightly, an economist at ING, noted: “There will naturally be some doubt lingering about these figures given they are telling such a different story to all other data on the labour market, but these are the official ones and on the face of it are fantastic. It suggests the American economy can bounce back very vigorously and we all need to massively revise up our economic projections.” FocusEconomics panelists expect the unemployment rate to average 9.8% in 2020, which is down 0.5 percentage points from last month’s forecast, and 7.8% in 2021.

REAL SECTOR

Labor market unexpectedly posts gains in employment in May Total non-farm payrolls surged 2.5 million in May, increasing at the sharpest rate since the series began in 1939, and baffled market analysts’ expectations of an 8.0 million decline. This follows April’s 20.7 million payroll cut—the starkest on record—driven by the Covid-19 pandemic and measures to contain the virus. Employment in the leisure and hospitality, construction and retail sectors increased notably in May, as containment measures gradually eased. The unemployment rate decreased to 13.3% in May from 14.7% in April, while the labor force participation rate ticked up from 60.2% in April to 60.8% in May. Hourly earnings fell 1.0% month-on-month in May (April: +4.7% month-on-month), while annual wage growth decelerated from 8.0% in April to 6.7% in May. Despite a positive reading in May, total non-farm payrolls are still down nearly 20 million since February.

Going forward, the labor market should gradually improve as lockdown measures continue to ease, but our panelists expect the unemployment rate will remain elevated for the remainder of this year. Commenting on May’s reading, James Knightly, an economist at ING, noted: “There will naturally be some doubt lingering about these figures given they are telling such a different story to all other data on the labour market, but these are the official ones and on the face of it are fantastic. It suggests the American economy can bounce back very vigorously and we all need to massively revise up our economic projections.” FocusEconomics panelists expect the unemployment rate to average 9.8% in 2020, which is down 0.5 percentage points from last month’s forecast, and 7.8% in 2021.