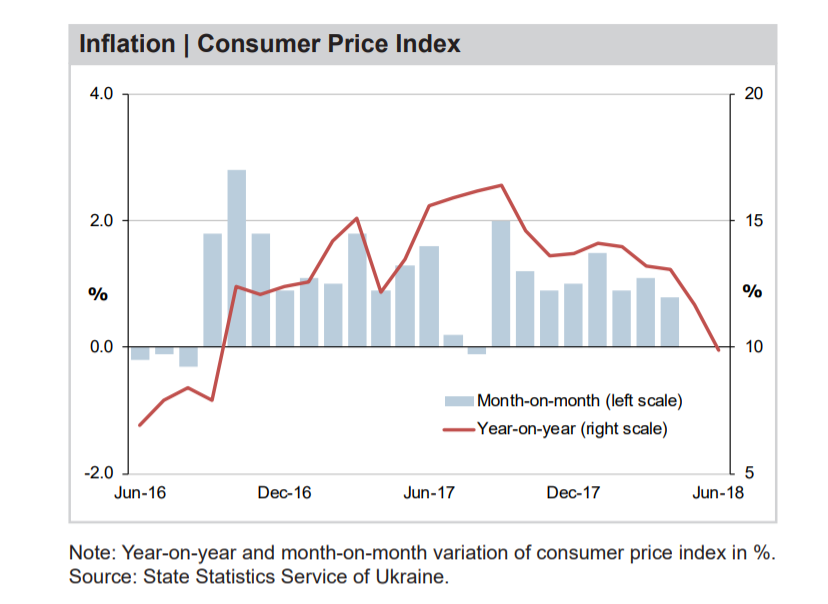

Ukraine’s recovery appears to have persisted in the second quarter, after growth picked up at the outset of the year. Domestic demand is expected to have remained in the driver’s seat in Q2: The sustained easing of inflationary pressures, coupled with improving labor market dynamics and strong remittance inflows, likely buttressed private consumption. In addition, household lending surged in the first half of the year against an increasingly stable banking sector. Meanwhile, the IMF has backed the country’s revised plans for an anti-corruption court after the amended law was approved by the Rada on 12 July. On a less positive note, in a move likely influenced by next year’s presidential and parliamentary elections, the government recently extended the gas-price freeze until the beginning of September, once again failing to fulfill one of the Fund’s key conditions and thereby reducing the prospects of receiving another tranche of funding in the coming months. • Domestic demand should remain healthy and lead the sustained recovery this year amid heavy investment activity and robust household consumption growth. Nevertheless, downside risks are significant and stem from mounting political tensions domestically and slow reform momentum. FocusEconomics panelists see GDP rising 3.1% in 2018, unchanged from last month’s forecast, and 3.1% again in 2019. • Inflationary pressures continued to ease throughout the second quarter, with inflation down to 9.9% in June from 11.7% in May, marking the lowest reading since September 2016. Our panelists expect inflation to remain elevated amid firm energy prices and recovering domestic demand. Inflation is seen closing 2018 at 9.3% and dropping to 7.2% by the end of 2019. • At its 12 July meeting, the National Bank of Ukraine unexpectedly hiked the key policy rate by 50 basis points to 17.50%. The decision came against the backdrop of heightened upside risks to short- and mediumterm inflation and elevated inflation expectations; a further rate hike in the second half of the year is unlikely. Our panelists forecast the rate to end 2018 at 16.30% and 2019 at 13.67%. • The hryvnia exhibited some weakness against the U.S. dollar in recent weeks. On 27 July, the UAH traded at 26.73 per USD, 1.6% weaker month-on-month. Nevertheless, since the beginning of the year the hryvnia has gained 5.1% on the USD and has been among the world’s best performing currencies this year. Our panelists see the hryvnia ending the year at 28.39 per USD and weakening to 29.75 UAH per USD at the end of 2019.